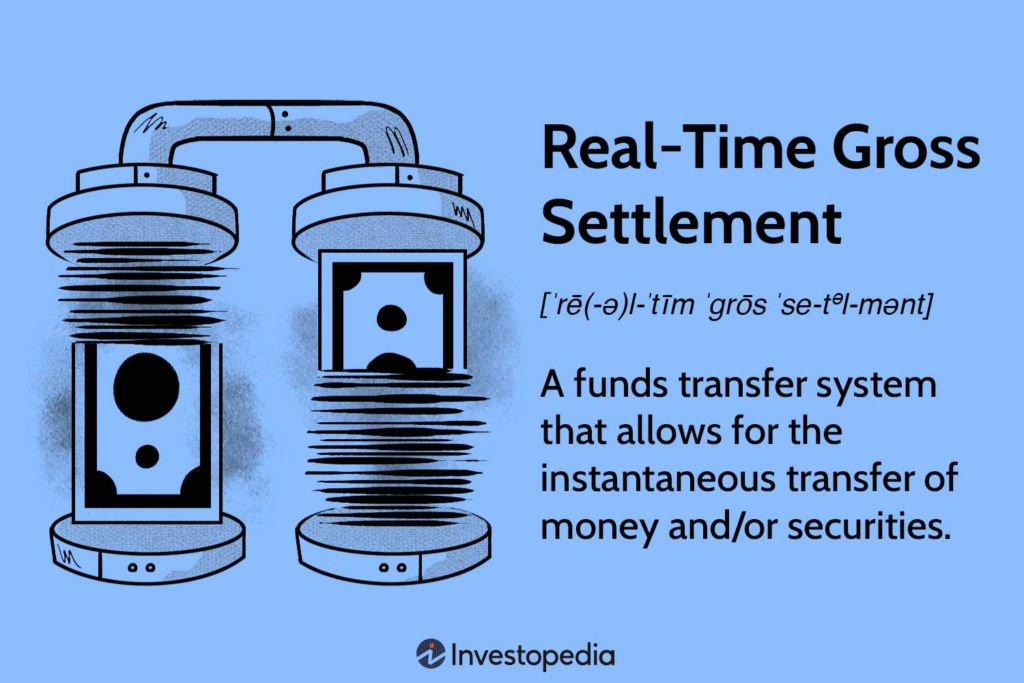

The phrase “real time gross settlement (RTGS)” is used to describe the fund transfer system which allows instant transfer of money as well as securities.

RTGS is an ongoing process that allows the payment of payments through single orders without the need to nett credit and debits on the books of central banks.

Once the real time gross settlements can be revocable and irrevocable. In most countries the system is run and managed by the central bank.

How Real Time Gross Settlement (RTGS) Works

RTGS (Real time Gross Settlement) inside banks is vital in making it more convenient and safer to move of money between banks and financial institutions.

RTGS can be used for transfers of amounts of more than two lakhs value subject to restrictions on transfers to third party accounts set by the client and specifically outlined guidelines an institution is required to follow.

RTGS transactions ensure quick and safe money transfers. They also increase efficiency in the financial industry.

The process begins when the sender RTGS procedure begins with sending party whos either person or business asking the their bank to deposit certain amount of cash into the accounts of the beneficiary at the bank of their choice. instructions can be sent via several methods like internet banking via mobile or via visit to branches of banks.

* The authorization and verification of the bank of the sender confirms there is sufficient funds in the accounts of the sender to make payment for the transfer amount. If funds are available and the bank has authorized transfer then it will be approved by the bank.

Transmission of instruction to RTGS system. When transaction is approved by the bank which issued authorization it initiates RTGS transactions by sending instructions to pay into the RTGS system. Most often the process is supervised and monitored by central banks.

* Central bank processing Central bank processing is vital function during the real time settlement transactions. The bank processes and gets information regarding the transaction making sure the transactions are in compliance with all relevant regulations and security requirements. Central bank also handles bank accounts for settlement of banks that are part of the consortium.

* Interbank settlement: Central bank debits the bank account of the senders settlement and then credit the bank account of the settlement account that is credited with the value of the settlement. This is essential in ensuring that transactions settle in real time and as whole which means that every transaction is settled on its own without netting any additional transactions.

* Notification of bank of beneficiary: the bank will be informed about newly received funds received from Central Bank. Notification triggers the payment of an account in the bank to the beneficiary based on sum paid.

* Crediting the beneficiarys account after receiving notice by central banks beneficiary bank quickly credit the funds in the accounts of beneficiaries and make the funds available for use.

Senders bank immediately provides confirmation to the sender that informs them that the RTGS transactions success. The confirmation provides both the sender as well as the receiver confidence that the funds were transfered in secure way and at the right date.

Record of transactions at the banks that send the transaction as well as the recipient maintain records of transactions for both bank customers. They are used as evidence for the transaction. The records are used to reconcile transactions or for auditing.

RTGS in contrast to. Bankers Automated Clearing Services (BACS)

The gross settlement in real time method is different to net settlement strategies that are comparable with UKs Bacs Payment Schemes Limited which was formerly known by BACS. Bankers Automated Clearing Services (BACS). Transactions between companies who use BACS are tracked throughout the time. When the day is over the central banks rebalance accounts in active usage based on the amount net of the funds transferred.

RTGS is not financial exchange. Central banks typically modify balances for both the sending banks and the sending one electronically. For example sending banks balance diminished by one million dollars while balance at Bank B recipient institution is raised by one million dollars.

Features and Benefits of RTGS

* Security and Safety RTGS is term with the RTGS description (Real time Gross Settlement) within the banking sector is an highly secure way of moving funds. Because its an electronic method of transfer it significantly decreases the chance of theft and fraud as compared to physical instruments such as checks and demand drafts.

* Limitless Real time gross settlement transactions carried out through banks branches generally do not have limit which makes it feasible to transfer massive or smaller sums of money through real time gross settlement.

* Real time transfers: RTGS is one of principal components of real time gross settlement. Banks are capable of providing real time money transfer. The account of the recipient is credit as soon as transfer begin and improves effectiveness.

* All week: RTGS operates on every day including holiday weekends as well as weekends together with real time gross settlement which gives users constant access to transfer money at any time theyd like increasing the convenience and accessibility.

*There arent any tangible instruments. real time gross settlement can be complete replacement for documents that are physical such as demand drafts or cheques because it is entirely electronic. Not only does it speed up processes but also reduces the risks that come to physical documents.

* Reduction of risk of physical instruments within RTGS drastically reduces the risk that the instruments could be for ride or cashed in illegally by non authorized individuals or groups which increases the security of the instruments.

It is convenient to use internet banking RTGS transactions that are part of the real time gross settlement systems are easily performed from the comfort of your home or at work through online banking. This ease of use provides flexibility and the ease of using electronic money transfer.

* No cost Although some banks be charged nominal costs for Real gross settlements in real time the most banks offer this service free of charge at nominal cost. This makes it cost effective method for transfer of funds within the real time gross settlement structures.

* Legal assistance: RTGS transactions being legalized and monitored in real time gross settlement provide users with feeling of safety and security knowing that transactions in financial institutions are secure by law thereby increasing confidence in the system.

How To Initiate RTGS Fund Transfer Online?

* Log into your bank account online.

* Enter to”Funds Transfer” or “Funds Transfer” or “Payments” section.

* Click “RTGS Transfer” as option to transfer.

* Enter information for beneficiary. Account number name of the beneficiary Bank information for bank information for the beneficiary (name as well as branch) together with IFSC code.

* Indicate the amount of transfer.

* Review and confirm the details of transactions.

* Transfer has to be authorized by method of authentication like OTP.

* You will receive confirmation of your transaction that contains reference codes.

* The recipient will be notified of funds when they arrive. In real time.

* Record confirmation data to be used in the future.

What Information Is Necessary to Begin an RTGS Transaction?

* is the name of bank which is the beneficiary as well as branch.

* The complete name of the recipient.

* IFSC code of the bank that receives the money from the bank.

* The value that is to be transferred.

* Notes that are relevant or comments If needed any pertinent notes or comments.

* The details of the account of the sender.

* The number of the account of the beneficiary.

RTGS Transaction Limits in India

The maximum for transactions using RTGS (Real Time Gross Settlement) is as follows:

* The minimum that can be transferred by RTGS of 2 lakh is. 2 lakh.

* RTGS Limit per day at the branch of bank: There is no upper limit set for RTGS transactions conducted by banks branch. Therefore you are able to conduct any transaction that is greater than the limits of. 2 lakh.

* RTGS Limit per day for online banking. If you choose to perform an RTGS transfer via online banking the likelihood is that you will reach limitation. Limits can be set by 25 lakh rupees. 25 lakh. It can differ between banks. Certain banks could have either lower or higher limit on online banking RTGS transactions.

RTGS Transaction Timings in India

RTGS (Real time Gross Settlement) Services are available 24/7 throughout the week which is inclusive of weekends and weekend holidays in India. You can have the possibility of making RTGS transactions any time and guarantees rapid RTGS transactions. Central bank debits the account for settlement of the sender and credit accounts of settlement banks which is credited for the amount of transaction. Additionally RTGS are used to transfer funds that exceed 2 lakhs of dollars according to the restrictions for transfers to third party that are set by the customer and any particular guidelines set by the institution.

RTGS Charges

RBI has reduced the costs associated to transfers that are made using RTGS transactions on the online. In the case of offline modes of transfers fees for RTGS transactions may differ between banks based on the size of the transaction. Some banks may offer lower RTGS fees for accounts with premium rates or certain customers.

Take note that the exact costs and the methods used to complete transactions may differ depending on banks that offer the RTGS service. You should confirm your banks details to ensure that you are using the latest and current data.

What Is Real Time Gross Settlement Fee?

The expense of real time gross settlement will differ based the location of the institution or country from which settlement is conducted and the size of the settlement. Some fees are removed at the discretion of the institution.

Different Modes for Initiating RTGS Transactions in India

Internet banking banks prefer web based banking solutions that permit customers to initiate RTGS transactions online. users can sign in to their bank accounts online and follow the directions their bank offers to finish RTGS transfer.

* Mobile banking apps The banks can also provide mobile banking solutions that enable users to perform RTGS transactions with the smartphones or tablets. Apps are user friendly and can be used to bank on the mobile.

* Bank Branch Customers can go to the branch of their bank to make an RTGS transfer right there. Bank staff will help in making the transfer and ensure the necessary details are provided.

Example of Real Time Gross Settlement System

An excellent illustration of an illustration of real time gross settlement could be whenever customer asks the bank to transfer money for different bank through RTGS and transfer happens instantly. Central bank is then able to debit accounts of the sending bank.

Then the banks the settlement account with the total amount. If the transaction was made by an automated clearing house (ACH) the transfer could require few days for clearing.

What Is Difference Between Net Settlement and Real Time Gross Settlement?

The difference between net settlement and to real time gross settlement (RTGS) is it is collection of information that is then sorted in order to settle by the close of every day whereas RTGS includes data for each transaction which are processed and settled at real time pace (processed and settled instantly).

Important Considerations for Initiating an RTGS Transaction

If youre making an RTGS (Real Time Gross Settlement) transfer. It is essential to remain alert and watchful to ensure security and the accuracy of your transaction. It is essential to keep in mind:

* Easily compatible with the network Check that the banks with origin as well as destination branches are included in the RTGS network. RTGS transactions can only be executed by banks that are members of the network.

• Information on beneficiary sure that you can verify the information of the beneficiary which includes the full name of account number as well as the type of account. Additionally you need to be able to verify the name of your beneficiary as well as IFSC (Indian Financial System Code) of the bank which is the branch of your beneficiary.

* For the security of an the account number is matter of care must be used when providing the accounts numbers of beneficiaries. RTGS transactions rely heavily on credibility of the data. Account numbers that are incorrect could result in the debiting of funds to an account that is not correct.

Documentation of the transaction Record the RTGS message or payment instructions. Records are utilized as evidence of transactions. Records can prove useful in the instances of disputes or contradiction.

* Bank policies Find out the specifics of your banks RTGS guidelines which contain limitations for transactions as and fees (if applicable) as well as any additional policies or guidelines may be in place.

In real time Gross settlement (RTGS) is vital element of the financial system. Its the one that ensures that interbank transactions are settled continuously and facilitates the immediate transfer of money or securities. RTGS technology minimizes risk for financial institutions in the event of high value transfers.

- What is Artificial General Intelligence (AGI) | Master Guide 2026

- Agentic AI and Autonomous Agents: Guide to the Next Evolution of Ai

- Options Trading Automation Using Python: Complete Beginner Guide

- Synthetic Data Generation: The Ultimate Master Guide 2026

- GitHub Copilot Master Guide 2026: The Ultimate AI Coding Handbook